Return to Financial Insight's main page.

![]()

The following are Financial Insight articles. Please note the dates at the top of the articles, indicating when the article was published, especially the first date published, as that would indicate when it was originally written. Remember that many were written a long time ago and while a lot of the advice is still unchanged, circumstances do change and therefore in some cases the advice today could be different.

Click on an individual article to jump to it, or scroll down through all the articles.

Computer Models: The Great Deception

Why Should Shareholders Pay Twice for Management's Mistakes?

We are Looking For Good Companies, Not Perfect Ones

Selling, One of an Investors Toughest Decisions

Are Prices High, Earnings Low, Or Something Else.

Buying and Holding Quality is Still Our Favored Approach

Before looking at PE's, Take a Good Look at Earnings

When Too Much Safety Increases Risk

Derivatives Should Be For Hedging, Not Speculating

How to Build a Stock Portfolio

To Lease or to Own, A Consumer Dilemma

Borrow or Pay? A Consumer Dilemma!

A Strategy for Fixed Income Securities

A Discussion on Mutual Fund Fees

Use a Mixed Approach to Build Your Portfolio

Price Targets Are Good For Brokers. But Are They Good For You?

In Defense of the Oil Industry

What Is A Mutual Or Investment Fund?

Stocks are Overvalued, Well Some of Them Are!

Are There More Mutual Funds Than Stocks

The Relationship Of Short Term Results To Future Returns

Selecting Equity Mutual Funds, A Quality Exercise

Is the Market Overvalued? What About Your Portfolio or Mutual Fund?

You Do Not Need A Fortune to Build A Diversified Portfolio

After The Dust Settles, It is Future Earnings That Count

Short-Selling; Risky Speculating, But Is It Investing?

The Stock Market, Bull, Bear Or A Number of Independent Companies

Small Cap Companies For Maximum Growth

The Big Multinationals, Maybe The Growth Companies Of The Twenty First Century

RRSP's & RRIF's: The Power Of Sheltering

Dave's Comments on the Recent Events of Bre-X

Buying On Margin For Bigger Returns and Bigger Losses

Diversifying, How Much is Enough?

Market Timing Can Improve Your Returns, But You Better Be Good!

Myths of Load Verse No Load Funds

The Canadian Government's 1998 Budget

TIPS & HIPS, An Alternative to Mutual Funds

There Is More To A Company Than Just Numbers

Some Portfolios Go Up During A Crash

The Emerging Markets, Big Winners Or Losers

The Other Way To Invest Internationally

Market Review and The Quebec Referendum

When Selecting Mutual Funds, Pay Attention To Management

Looking For Quality Equity Mutual Funds

RRSP's and Shelters, Which Investments Should You Shelter

After Considering Inflation, Interest Rates Seem Pretty High

![]()

Published: November 25, 2014

Like many tools, when used properly computer models can be a great aid. They allow us to efficiently run what if scenarios and make some useful comparisons. In the investment world, these kinds of analysis can be very helpful. We even have one that is available free on our website, IFC Stockvaluator. It is a wonderful tool that helps us evaluate different stocks. It allows us to see different ratios, their trends, to chart different growth rates and to calculate an intrinsic value of a stock. This can be very helpful when kept in perspective; it can also be very dangerous if overemphasized.

There are two glaring weaknesses in any model. The first more obvious one is the old garbage in garbage out rule. If the data you input is not correct, well then neither is your output. The second less obvious weakness is that if the model does not correctly identify how different parameters interact (or omits important parameters) then the results will be wrong regardless of how good the inputs are.

So let's take a look at Stockvaluator. It calculates an intrinsic value of a stock based on one very important premise. It assumes that a stock is worth the discounted value of all its future earnings. We believe that is what a stock is ultimately worth. If however, our assumption is incorrect, then all bets are off. We would argue that while many things affect a stock's price, at the end of the day, it usually comes down to future earnings. If we are right we may have a useful tool, if not then we have a disruptive tool. Of course, even if our premise is basically right, if we do not correctly get how the variables interact, or miss some important variables, then even if the calculations are perfect our results will be wrong. Then there are the inputs.

In the case of Stockvaluator, there are several inputs that you have to enter after reviewing the company's ratio and earnings history. First there is the earnings per share starting point. This may seem simple, but maybe the current year is an anomaly. Then there are the growth rates. Crystal ball anyone. Finally there is the discount rate. You may know what you expect but what does the market expect and how quickly that can change.

So you might ask why we use this modeling tool. Well, it does allow us to run what if scenarios, for example, what if we raise or lower the discount rate, or what is the effect of different growth rates. We can also compare our results to what the market is telling us. Does the stock appear to be of good value, or are the differences significant and maybe we should have a lot more questions? Again, a great tool when used correctly and we do not over rely on it. This brings us back to our title, The Great Deception.

If you watch the investment press or listen to many if not most brokers and portfolio managers, it seems as if no one wants to do their job any more. Instead of doing the work of carefully analyzing companies and building solid portfolios of high quality companies, everyone is looking for a short cut. They seem to believe that they can create these computer models that will identify key factors and move in and out of stocks or markets and thus outperform them. Well, if you build enough different models, some will work, some of the time, sometimes for quite a while, but none will work all the time and some will build your confidence before letting you down in a big way.

While models have a place, they are just a tool. The world is just too complicated and it is constantly changing. There is no way that any model can take into consideration all or even most of the different parameters, know what they will be and how they will interact with one another. Yes, you can figure what would have worked for the previous year, maybe even decade, but nothing stays the same. We have no doubt that many if not most of the people building and promoting these models really believe that their models will work. Maybe after all their time and effort, they need to believe it. Maybe that is the Greater Deception. But do not be taken in, when it comes to something as complicated as the investment world, Computer Models are a tool, one of many, nothing more, nothing less.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: 2012

There is an old Accountants/Auditors joke. I first remember hearing it in 1978 when I was a young Auditor with the Office of Auditor General of Canada. It goes something like this:

People are being interviewed for a job. The first one is asked the question "What is one plus one." The applicant frets over it a minute, it must be a trick question. But finally answers."Two." The second applicant is also asked "What is one plus one." This applicant also frets over it a minute, it must be a trick question. But finally answers."Two." The final applicant is an Auditor and is asked "What is one plus one." The Auditor thinks a minute, then thoughtfully answers. "What would you like it to equal?"

There is the old adage that numbers do not lie. Maybe not, but they can certainly be misleading. The same goes for statistics, charts and rules, if they are not applied correctly. In this case I am going to discuss charts.

Following are a number of charts showing investment returns. Take a minute and have a look. Which ones do you like?

So which ones look good? At first glance, would you say that Chart B (top left hand) looks like a pretty smooth but only slightly upward return, Chart D (top right hand) is downward, while Chart A (bottom left hand) goes up but is very volatile and that Chart C (bottom right hand) has a nice steady upward trend?

Now look more closely. Would it surprise you to know that all of these charts represent the return of my personal portfolio? That's right, these are all different representations of the same portfolio, yet at first glance they each seem to tell a different story. All I did was play with the scales and the time frame. Which one someone shows you might depend on what message they want to convey.

Chart B is a log chart of January 1 1998 to December 31, 2011 (14 years). Normally I like log charts, as they make a straight line a straight line. That is they adjust the scale as the values increase which removes the distortion of an investment with a steady return taking off. Let me explain. On a normal chart, a 10% return on $1,000 is $100 while on $10,000 it is $1,000. Therefore, a constant 10% return looks steeper as the value increases. So on a regular chart the current returns can look better or more volatile than older ones only because they are on a larger scale. On a growing portfolio, a logarithmic chart removes this distortion and can be more meaningful. Chart A (below chart B), is the exact same data, but on a normal chart. The problem with Chart B is that because scale is so large it has flattened out everything and is hard to decipher. The problem with Chart A is that the more current numbers look more volatile because for example a 25% drop on $3,000 is 3 times larger than a 25% drop on $1,000. Below I will show a better logarithmic chart but for now let us move on to Charts D and C.

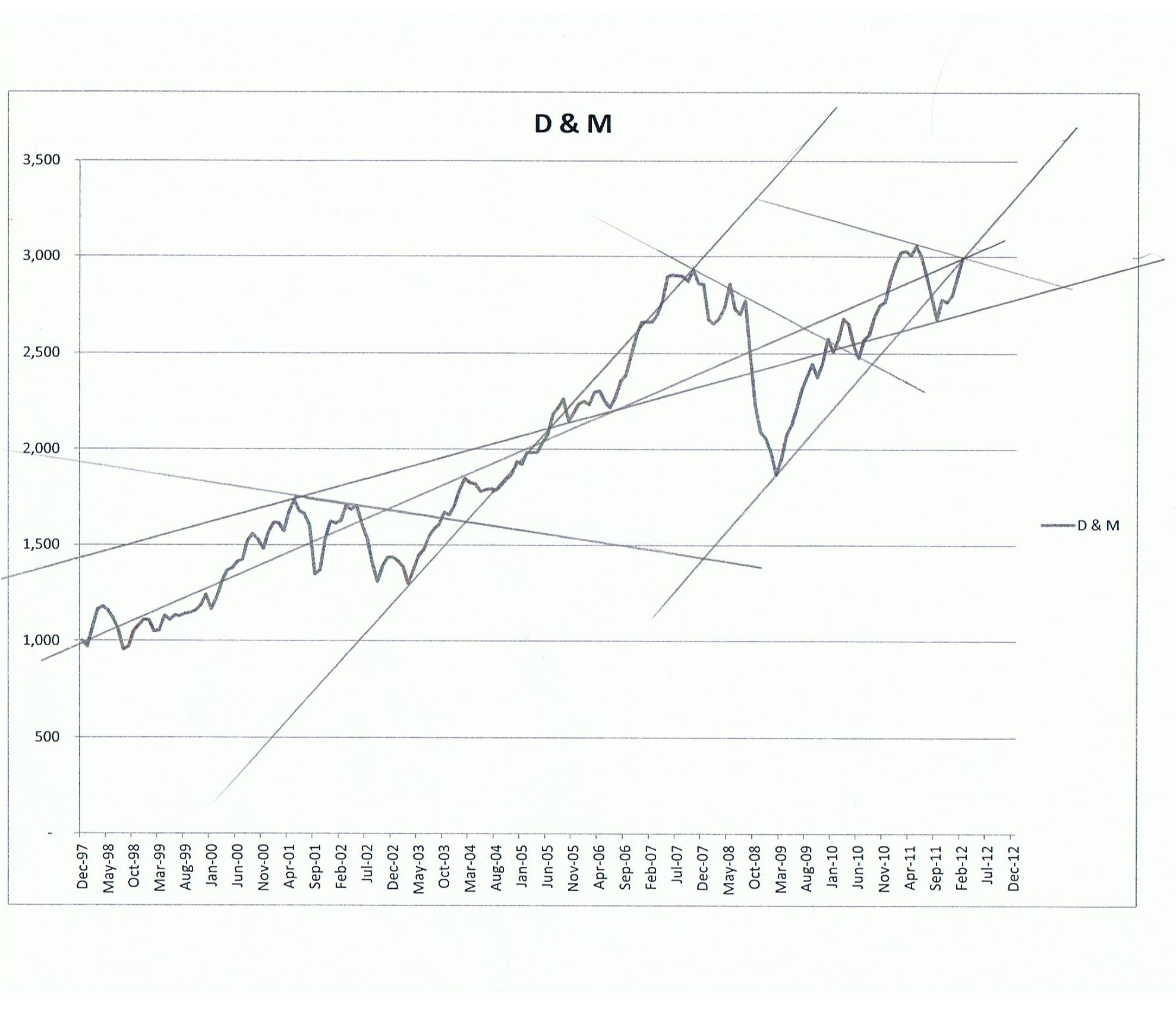

If you look closely at chart D you will note that it goes for the relatively short period of May 2007 to February 2009 while Chart C goes from a little longer period of May 2003 to September 2007. If I want to brag, I would show you chart C, steady growth with minimum dips. If I want to scare you I would show you chart D and tell you how the stock market is for losers.

Now for emphasis below is Chart D&M It is really the same as Chart A but with a whole lot of trend lines drawn through it. As you can see, by carefully picking the period, I can really change the story.

Of course charts can be helpful. Below is Chart E, the one I like. It covers the whole 14 year period, but it is a logarithmic chart and of a useful scale.

This is a much more representative chart. The period is long enough to be meaningful, the scale is such that you can see what happened and the later ups and downs can more easily be compared to the earlier ones. You might say that it shows a pretty good long term trend where losses happen but are made back and then new gains are made. You could also say "you can run, but you cannot hide." That is to say, the overall trend is good but while the volatility is not distorted to look greater than it is, it is also there and clear to see.

Charts and graphs are used in many disciplines and are a valuable tool that helps us to interpret data. I use them all the time. However, whenever you look at one, whether it is financial, statistical, a voter poll, weather, climate or anything else for that matter, you need to look at it with a degree of skepticisms. What are the scales, should it be logarithmic, what is the range, what is the margin of error, are you looking at the right or relevant information, how can this be misleading and finally, of course, how can this be helpful in decision making while not being misleading.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: January 2001, March 2003, Mid 2012

Note: This article was written several years ago before TFSA's became available. While it has been modified to reference TFSA's, it is mainly about RRSP's even though both have similar sheltering benefits.

Why RRSP's Work

It seems that every so often there has to be some discussion on the benefits of RRSP's. Someone will question if equity investments even belong in RRSP's since the tax on Capital Gains is much lower than on normal income. Their premise is that since capital gains are only one half taxed, it may make more sense to leave the investments outside of the RRSP. After all, withdrawals are fully taxed, so you lose some of the benefit that is afforded capital gains. We must admit, a few years ago when the rates were dropped back to 50% of the normal rate, we had our questions too, so we did do some analysis.

On the outside, many of the arguments sound good. However, as is often the case, these discussions fail to grasp the complete picture, so we ran some numbers. We figured that there was some basis to the argument that since the money in the shelter would be fully taxed when it was withdrawn; maybe it should be left outside. Actually, we assumed, wrongly assumed, that it would take some time for the benefits of sheltering to outweigh the benefits of the lower tax rate. What we found was that the advantages of the shelter took effect as soon as there was any, we stress any, realized return on investment. We had to give that some thought, but once we remembered that RRSP's are bought with before tax dollars where other investments are bought with after tax dollars, the answer became clear.

Since the money is going to be fully taxed anyway, either when earned or when withdrawn from the RRSP, it is what happens in the middle that counts. Since the RRSP shelters the income in the middle, it is better. Let us explain.

One of the first things that is often forgotten is that a rear-end load on the final balance has exactly the same effect as an equivalent front-end load on the original balance. For example, say you were investing $1,000 in an investment that would double in five years, and you had a choice of either a 10% front-end or a 10% rear end load. It would not make any difference which option you chose. With a front-end load you would get an original net investment of $900, once it doubles you have $1,800. With the rear-end load you start with the whole $1,000, once it doubles you have $2,000 then you pay the 10% rear-end load of $200 and you have the same $1,800 left over. In this way, RRSP's and TFSA's provide similar tax advantages.

The same principle applies to RRSP's. Outside an RRSP your original income, which is how you got the money to invest in the first place, is fully taxed at the beginning, like a front-end-load. However, if you put the money into an RRSP, the tax effectively becomes rear-end loaded instead. As we showed above, there is not really any difference in the end. However, with the shelter, in a way, the income in the middle is not taxed. Let us give you an example.

Say you are in a 40% marginal tax bracket, and for simplicity sake (and lack of a better assumption) you will always be in a 40% marginal tax bracket. This means that every additional dollar you earn is subject to 40% or 40 cents in taxes. Now lets assume that your employer gives you a $1,000 bonus that you plan to invest either inside or outside of your RRSP at a rate of 10%.

If you put the money into an RRSP, you can invest it all, as it will not be taxed. Also inside the RRSP the income is not taxed either. So at the end of 10 years you will have $2,594. If you then withdraw the money, you will pay 40% taxes on the balance and have $1,556 left over. Or you can invest outside of the RRSP.

In this case, the original tax is front-end loaded instead. That is you receive $1,000 but must immediately pay $400 in taxes. So now you have $600 to invest. Of course this is not a problem, since there will not be a rear-end tax, and we have shown that the effect of a front-end load or tax is the same as the rear-end load or tax. Except for one thing, outside the RRSP, the income is also taxed as it is earned. This means that if in the first year you make 10% or $60 ($600X10%), the government gets $24 of it and you keep $36. So your after tax return is only 6%. At 6%, in ten years your investment is worth $1,075. True there are no more taxes, but the $1,556 (calculated above) that you are left with after withdrawing from the RRSP is significantly better than the $1,075 you get to keep if the money is outside your RRSP. The difference is because in a way, inside the RRSP the investment income was tax free, as you really only got taxed on the original investment (albeit, on the final balance instead of the original balance). Of course the difference is less if you invest in investments that earn capital gains instead.

If you had invested in stocks that only returned capital gains, (no dividends), then outside the RRSP only 50% of the gains would be taxed, meaning an effective tax rate of 20% in the example. Also, the tax would only be due once the gains were actually realized. So if in the example you held the stocks for 10 years, then there would be no advantage to the RRSP. However, if every year you realized the return (presumably because you flipped the stock) then the RRSP has an advantage. In that case, your return would be reduced to 8% (10% less 20% of the return for taxes) and at the end of ten years you would have $1,295. Still significantly below the $1,556 you would have kept by using the RRSP. While we agree that you are not likely to flip the whole portfolio every year, especially if you follow our advise, it stands to reason that from time to time you will be flipping some investments and eventually you will probably be realizing most of an average years return every year. For example, if you turn over 20% per year, that suggest that every 5 years you will flip the equivalent of the entire portfolio, and after 5 years each year's realized income, which will be taxed, will equal one average years income. Regardless, while the difference may be less than what we are showing, the advantage of the RRSP is still there and is still significant.

It is worth noting that while the calculation is different for TFSA's the results would be the same.

It seems fairly obvious from the above that we should use RRSP's and TFSA's as much as possible.

The following table shows the difference in the value of a $1,000, 4% interest bearing investment after all taxes after 1, 5, 10, 20, and 25 years assuming a 40% marginal tax rate. Remember, outside the RRSP the money was taxed when it was earned, so you would only have $600 to invest to start with.

Description |

Value After 1 Yr. |

Value After 5 Yrs. |

Value After 10 Yrs. |

Value After 20 Yrs. |

Value After 25 Years |

| Inside RRSP | $624 | $730 | $888 | $1,315 | $1,600 |

| Outside RRSP | 614 | 676 | 761 | 964 | 1,086 |

| RRSP Advantage | 1.6% | 8.0% | 16.7% | 36.4% | 47.3% |

The following table shows the difference in the value of a $1,000, 10% capital gains type of investment after all taxes after 1, 5, 10, 20, and 25 years assuming a 40% marginal tax rate resulting in 20% taxes on the Capital Gains. Again, remember outside the RRSP the money was taxed when it was earned, so you would only have $600 to invest to start with.

Description |

Value After 1 Yr. |

Value After 5 Yrs. |

Value After 10 Yrs. |

Value After 20 Yrs. |

Value After 25 Years |

| Inside RRSP | $660 | $966 | $1,556 | $4,036 | $6,501 |

| Outside RRSP | 648 | 882 | 1,295 | 2,797 | 4,109 |

| RRSP Advantage | 1.9% | 9.5% | 20.2% | 44.3% | 58.2% |

As you can see, even after a year there is an advantage to the RRSP. There are cases where you do not want to use an RRSP however, but you should examine them carefully before you decide.

One reason is because you expect your tax rate to go up in which case a TFSA might be a better choice. In an RRSP this is a risk, although maybe less than it used to be. However, unless you expect a pretty significant increase and do not expect to leave the money invested for a long time, we think that the value of the shelter will probably more than make up for any difference. So do some analysis. The investment may be of a short-term nature, as you have plans for it. In this case the money should be kept outside of your RRSP's but it might be worthwhile to put that money in a TFSA if you have room. You may have investments that do not qualify. Obviously these investments must be held outside your RRSP's. Another reason is because you want to keep your high-risk investments out of your RRSP's. This makes sense, as it is wise not to gamble with your retirement funds. On the other hand, if you hold these investments anyway and you have additional room to put them into your RRSP, then it might be a good idea. It could be argued that if they go bad then you lose the ability to deduct the loss. However, we note that until you take the money out, it is in fact 100% written off inside the RRSP, which beats only being able to deduct 50% of it from other capital gains. On the other hand, we would recommend that if there is any chance that this high-risk investment is using RRSP room that you might one day want for another investment, then it is probably best kept outside your RRSP, and you might be surprised at how much money you will have to contribute one day, especially after the mortgage is paid and the kids are gone. This leads us to the last reason that came to mind. No more RRSP room. If you are investing more than what you can contribute to an RRSP, (which we would encourage), than something will have to be outside of your RRSP's. And that leads us to the question of which investments to place inside your RRSP's.

Which Investments Go Into an RRSP?

There are continuing debates on this issue. As we have pointed out, it is usually wise to use the RRSP shelter as much as possible. However, if your investments are larger than what you can have in your RRSP's, then some will have to be outside. The goal is to have the most money after all taxes at the end of the day. Sort of like; “He who dies with the most toys wins.” There are two common positions on this. The first is that you should shelter the investments subject to the highest taxes first. For example, interest income is taxed at a higher rate than dividends and capital gains, so under this argument, you should put your investments that make interest income into your RRSP first. The other argument is that it is better to shelter your highest returns. Until recently, we mainly agreed with the second argument, as our analysis had shown that the value of the sheltering of the larger return outweighed the difference in the tax rates. This was assuming a long-term return of 10% on equities and 4% on fixed income securities plus the tax rate on equities was about 2/3's that of the rate on interest. We found that after about 20 years, the benefit on the equities was so good that the RRSP made sense even if there was not a deduction for the original contribution. However, with the tax inclusion rates of capital gains being lowered back to 50%, the balance has shifted.

The following table shows the value of two investments, added together, after 5, 10, 20, 25 and 30 years. In each case the investor invested $1,000 in stocks earning (and realizing) 10% capital gains per year and another $1,000 in an interest bearing investment returning 4% per year. The investor's marginal tax rate is 40%. In the first instance the stocks are in the RRSP while the interest investment are outside. In the second case, the interest investments are inside the RRSP's and the stocks are outside.

Description |

Value After 5 Yrs. |

Value After 10 Yrs. |

Value After 20 Yrs. |

Value After 25 Years |

Value After 30 Yr. |

| Stocks inside RRSP | $2,092 | $2,824 | $5,643 | $8,310 | $12,507 |

| Interest Security Inside RRSP | 2,199 | 3,047 | 5,976 | 8,448 | 12,009 |

As you can see, it takes almost 30 years before it is better to have the stocks inside the RRSP instead of the fixed income securities. Of course the changeover point changes depending on what assumptions you make regarding returns, tax rates, amount of dividend income, how much natural sheltering you get from a buy and hold strategy and so on. But it seems safe to say that it now takes some time before it is better to have the stocks inside the RRSP with the fixed income securities outside. Therefore, unless you expect to have the investments in your RRSP for over 30 years, it is probably best to but the fixed income, or interest bearing securities into your RRSP first then add the equities until your room is used up. These analysis also apply to TFSA's, so look at your whole mix.

Conclusion

Based on our analysis, there seems to be little doubt. Even with the lower capital gains rates, a Canadian investor should use RRSP's and TFSA's as much as possible. If their total investments are greater than the maximum that they can have inside their plans, then there are issues about which investments should be inside versus, which should be outside. However, it is clear that RRSP's still work, and even better than you might have thought.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: January 2009

The new Tax-Free Savings Account (TFSA) introduced in the 2008 federal budget and taking effect on January 2, 2009 are considered to be the most significant new savings vehicle in Canada since the introduction of the RRSP. This new vehicle offers an equal opportunity for tax sheltered savings to all adult Canadian's, regardless of income or age.

Details can be found on the Federal government web site at www.tfsa.fc.ca. Essentially they work as follows:

These new accounts should be a terrific savings vehicle and we expect that they will be used by many Canadians. How you use them will depend on your circumstances. Essentially they have the same real benefits of RRSP's but with added flexibility. See the article below about RRSP's that explains the benefit of sheltering. If you are a high income earner then you will likely want to contribute to RRSP's first and then put any amounts over your maximum RRSP contributions in a TFSA, or if you do not have extra funds you may put short term money in a TFSA instead of a regular savings account. If you cannot contribute to an RRSP (e.g. you are retired and over 71) then you might put some of your investments in a TFSA. If you expect to be in a higher income group when you retire, you might invest in a TFSA first, then into a RRSP. Many people will use the account as a good place to place savings that they want to keep available for future use. Especially in the first few years until they have built up contribution room. Of course there are many different situations and circumstances so you need to use the accounts in the way that works best for you.

We should point out a couple of other considerations. As with RRSP's, the quality and risk associated with your investments has nothing to do with the tax status, it is a result of the risk associated with the underlying investments. Also, it is worth verifying what service charges the financial institution in question will be assessing, especially while the amounts are smaller. There is no point in saving taxes only to have the savings eaten up by the financial institution. For example, $5,000 at 2.7% will earn $135 in the first year. If you are in a 40% tax bracket, the tax on that is $54. So in that specific situation if you are going to incur an extra $54 in service charges, then essentially the benefit of the shelter is lost. So, consider what the service charges will be.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: January 2004

What we are talking about is spin-offs. That is where a company takes a part of its business that is not as profitable or no longer fits into its strategic plan, turns it into a separate public company (if it is not already) and distributes the shares to the shareholders. There can be several formats for this: At one extreme there is the splitting of the company into two or more major parts (which is often a sound approach) where shareholders hold all the parts. The other extreme is splitting the company into two or more parts where insiders or majority shareholders get the good parts and the other shareholders get stuck with the rest (obviously a rare but very offensive occurrence). Then there is what we consider the more common action of spinning out a small part of the company as a separate company and distributing it to the shareholders. This last item is what we are going to discuss.

There is usually a logic to these spin offs. Normally the company has determined that a certain part of the business no longer meets its strategic objective, for whatever reasons. This may be because things have changed or because management made a mistake. To be honest, it does not matter; after all if management does not make mistakes, they are not doing their job. However, this section, division or whatever no longer belongs and it is fair for management to dispose of it. Usually this results in it being sold off in one form or another. However, sometimes management theorizes that the assets belong to the shareholders and it is only fair to give the assets to them and preferable without triggering a tax consequence. So they organize a spin-off and give the part being disposed off back to the shareholders in the form of shares of another company. Now this may be for selfish or for purely altruistic reasons but the end result is the same.

The shareholders are now holding a position of the original company (that is okay) and a small position of the new company that they likely never asked for nor especially wanted. It really does not matter what the size of their holdings are, if we assume that an individual had a reasonable position of the original company where the value of their shares was reasonable in relation to the rest of the portfolio, then chances are that relative to the rest of the portfolio, they have a tiny little holding of the spun-off company that they must deal with. We fail to see the benefit to the average shareholder in that. We believe that management has several better alternatives open to them.

The obvious solution is to simply sell the new company either through a share offering or though a private deal. If the spun-off company is to be a public company and management wants to give the shareholders an opportunity to buy the new company, then all that they need do is give them first crack at the offering. Once the spun-off company is sold, if it wants to benefit shareholders directly, it can issue a special dividend, or if it wants to avoid tax consequences to the shareholders use the money to repurchase shares, reduce debt or fund expansion, all of which are for the ultimate benefit of the shareholders and none of which will leave them holding a small position in a company that they never wanted anyway. While this complaint is valid, you might ask what you can do about it.

Unfortunately there is little a smaller shareholder can do about these spin-offs but they do have choices. First, we are starting to have an inclination towards selling or avoiding company's that are planning spin-offs. While we would not sell a favorite holding because of it, we did recently dispose of a company that we had become somewhat neutral on and where the sale freed up funds for purchases of some other companies that we liked better. We would not suggest that you sell a company because of a spin-off; however, it might be one of many factors that influence your decision. Another thing you can do if you hold a company that is planning a spin-off is if there is a shareholder vote, vote against it. Also, you can write to the company (probably addressed to either the Chairman of the Board, CEO, President, Investor Relations Department or all the above) and tell them that you do not approve of the spin-off. If you use a full service broker, complain to the broker, while they cannot do anything directly, if they are hearing a complaint from their clients, they may pass it on, and if the brokerage houses do not like an action, they can exert some pressure on companies that are considering spin-offs. Finally, talk to other investors and get them to complain to their brokers, acquaintances etc., because while one lone voice in the dark may not amount to much, the voice of many will eventually be heard.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: July 2003

No matter what company you are looking at, it is bound to have something wrong with it. This is something we are often reminded of when we mention some of our favorites. We say that we like a company and someone says the typical "Yes But?" They will bring up some negative issue and say how they are avoiding it because of this issue. The interesting thing is that about half the time it is something that we consider positive, as few things are crystal clear in business. The company might be criticized for taking a certain action. Of course, management thought this was a good thing to do, but obviously some investors disagreed. In these cases it is necessary to draw your own conclusion. We often find that we are in agreement with management. This might be because we are looking at a longer term than other investors, because we have a bias toward the company or maybe we just see it differently. Then again, sometimes we agree that it is a negative, or are not certain, but we realize that based on the big picture, the issue is not that important. Actually, believe it or not, these negatives often work to our advantage.

Sometimes these things have an adverse effect on the stock's current price. That is, the current price drops, often in an overreaction. When this happens, if we think the item is positive, or not really important from a big picture point of view, we may see it as an opportunity to increase our position, if our holdings are not to large in the first place. If we already have a significant position, then we may do nothing, and in the long run this temporary setback is just a fact of life, but not really important as we have no plans to sell in the immediate future. However, in one, five, ten or even more years from now, this item will be long forgotten and its impact negligible, if there is any impact at all. So the item worked for us or just did not really matter.

The point is, the above scenario is true of all good companies. No company is perfect. At any given time there is bound to be something wrong. Further, every good company has it ups and downs, so there will be times that a company gets beat up. This maybe a good thing as it provides buying opportunities. So our goal is to locate, buy and hold (for years, maybe decades) good companies. Not perfect ones, these do not exist, and if a company does appear to be perfect, well you might have to question that too. Then we build a well-diversified portfolio of these companies. We are human, and our information is not perfect, so sometimes we will be wrong. We will do our best to dump companies quickly when we determine that we were wrong and that the company is not of the quality that we once thought. But overall, with patience, in the long run, we should be right often enough to be rewarded with a respectable return. And that is a realistic goal.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: June 2000, March 2003

Deciding when to sell a stock is probably one of an investor's toughest decisions, and in our experience, the area where we are most likely to be wrong. When you consider that markets rise about seventy percent of the time, it seems likely that our sell decisions will be wrong more often than not. Taking that into account, it is easy to see why a buy and hold approach is usually the best. After all, if you buy quality, then it is fair to say that in the long run, most of your buy decisions will turn out to be good ones, while most of your sell decisions might turn out to be poor ones. Regardless, for every investor, there are bound to be times when they need to sell.

So how do you make those critical sell decisions? Do you follow a formula, stick to some fixed rules or use some other criteria. There are many theories, so finding an approach is not difficult. Then again, avoiding poor reasons is another matter. Below we have indicated some of the common reasons for selling and made comments on each. In our opinion, some are valid, some are not and some can be valid in certain circumstances.

Common Reasons to Sell:

Quality of the Company: The company no longer demonstrates the quality that you thought it had. This is probably the best reason to sell. Circumstances may have changed, or you may have realized that you made one of those inevitable mistakes. Regardless, once you realize that the quality is not there, it is time to cut your losses and move on.

Ideally, once you reach this realization, you should sell immediately. We must admit that we do not always do that ourselves. In some cases, by the time we realize that we were wrong (or maybe admit that we were wrong), the price has deteriorated so much that there is no longer any point to selling, as we would not realize much cash. In those cases, we are inclined to hang in there, as there is no longer much down side. If things turn around, then we are inclined to sell while the selling is good. However, usually when we change our mind, it is not after a price crash, so selling immediately is the best move.

Portfolio Clean Up: Sometimes we notice that over time we have accumulated a number of small holdings that are cluttering up the portfolio. The reasons for purchasing the stocks may have been valid, however, they may not be much more than clutter now. You might say that these are small holdings and why not let them ride. While this is true, they may also be diverting some attention that would be better spent elsewhere, and in that sense, they might be doing some harm. So it might be best to sell these stocks so that you can concentrate your efforts elsewhere. In this case, we would be inclined to revisit the stocks, reconsider why we purchased them in the first place, and then make a decision.

You like another company better: Another valid reason. Some selling is done to free up money so that we can buy other companies. In this case there are a couple of pitfalls to watch out for. First, remember to watch your mix. If you start selling companies in one sector to buy those in another, your portfolio might not be properly diversified across the different economic sectors, or geographically. So remember to pay attention to your overall mix. Second, while it makes sense to switch companies from time to time, remember that every time you do, there are costs. There are broker's commissions, losses from the difference in the bid and ask spread and lost opportunities from not giving an investment enough time to perform. So watch yourself to be sure that your switching (or trading), is to make minor adjustments from time to time and that it is not becoming a habit.

To rebalance your Portfolio:This is something that we all need to do from time to time. Within the stock portion of a portfolio, some stocks will significantly outperform the others. Also, within the whole portfolio, stocks will usually outperform your fixed income investments, which means that over time your portfolio is likely to become overweighed in stocks.

First there are the individual stocks that have grown to the point that you are overweighed in them. This can be tough; after all, one might argue that you should hang on to the best stocks. However, every company carries its own risks, which can cause it to suffer severe set backs or go out of business. So you should evaluate if you are overexposed in that stock. If you are, then it may be wise to reduce your holdings. When you are done, it may still be one of your largest holdings, but your balance will be better.

The other rebalancing has to do with reducing the proportion of stocks. Here, you will become aware that you are overweighed in stocks. At this point it makes sense to review your portfolio and select some stocks to either sell, or to trim. These rebalancing actions can be done slowly as opportunities present themselves.

Overvalued Stocks: You believe that the market has overvalued a stock for whatever reason. We would warn against selling a stock just because it seems to be overpriced. First, your valuation might be miscalculated for any number of reasons. Second, many of the best growth companies are overvalued all or most of the time, as they tend to be a little ahead of themselves. On the other hand, if you feel that a company is grossly overvalued, or are questioning its quality, then this might be another reason to sell the stock or reduce your holdings, but be sure to look at the whole story.

Your Cash flow: If you need cash, then you may have to review your portfolio and pick some stocks to sell or trim, to raise the cash. Obviously this is not what you want to do, but sometimes circumstances dictate. If possible, you should plan to have money out of the market well (preferably years) before you need it, so that you can slowly sell off stocks as opportunities arise.

To take profits: They say you cannot go wrong taking a profit. We are not sure who THEY are, but we must strongly disagree. Selling to take a profit may make your broker rich, but for you, it is more likely to create missed opportunities. Good solid companies with growing profits and share price, have a tendency to continue to grow. So if you sell after making a profit, you may be selling before the biggest gains are made. Also, once you sell the shares, you need to find somewhere to put the money. So if you are selling to take a profit, chances are you do not have a better place for that money. In which case, why were you selling?

You trade to a fixed formula: There are many formula's available to determine when to sell. One age old formula is to sell a stock after it goes up a fixed percent like 15% or down a fixed percent like 10%. Of course in a volatile market like today's, you are likely to sell most of your best stocks at a loss before they have a chance to go up, and you will never enjoy the real fruits of your best choices. Another formula used mainly for more speculative stocks, is to sell half of your shares after the stock doubles, this way you get your money out. While we agree that there may be some wisdom in getting some or all of your money out of your more speculative stocks, these should only make up a small part of your portfolio, and we think that formula's in general fail to realize the complexities of the world and consequently the complexity of the companies that you are investing in.

It hit a price target: This seems to be one of the more popular approaches. Setting price targets, then selling once the target is reached. Actually, we suspect that it is most popular with brokers, after all, once a target is hit, they get two commissions, one for selling then another for buying whatever you replace the old stock with. However, we see a lot of problems with price targets. First and most importantly, they assume a static world, but the world is anything but static. Also, they seem to oppose the buy and hold strategy that we continually recommend. Finally, once you sell, you have to find something to replace the stock with. If there is something better, then switch, do not wait for a target, and if there is not something better; then why did you sell the stock in the first place? Surely not so you could just buy it back, at what is likely to be a higher price. On the other hand, if you do not like the stock, then sell it; do not wait for a target that might never be reached.

Price Maximized: You think that your stock has gone as high as it is likely to go. Well okay, but why is it that you think it is unlikely to go any higher. Is it to do with the company's quality, or are you just market timing. We already addressed the quality issue, if the quality is not there then sell, however, if you are trying to time the market, chances are that eventually you will learn that the market is smarter than you. We can say categorically that the market is smarter than us. This should not come as a surprise as most of the most successful investors like Warren Buffet and Peter Lynch, to name a couple, continually stress that they cannot successfully time the market.

To time the market: Okay, we will say it again. If you are trying to time the market, chances are that eventually you will learn that the market is smarter than you. We can say categorically that the market is smarter than us.

To rotate to the next winner: This is another form of market timing. So our comments on the last two reasons apply here also.

To make your broker rich: This may not be as humorous as it sounds. While we believe that most brokers genuinely do look out for their clients best interest, there are some who are more interested in lining their pockets with commissions than in looking out for their clients best interest. While we cannot prove anything, during tax time, even during bull markets, in the tax part of our business, we do sometimes notice cases where the brokers seem to be making more on commissions than the clients on the investments. In these cases, you really have to wonder what is going on.

The Final Decision:

You may be wondering which approach to follow. However, we do not prescribe to any hard rules. Sometimes you will sell a stock for one of the above reasons, more often than not, it will be for a combination of reasons. The trick is to know what your reasons are and understand the difference between good and bad reasons. Then you should make the best decisions you can and move on, putting those decisions, some good and some not so good, behind you.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: October 2002

To answer these questions in order: Not necessarily, yes and yes. It is interesting how when markets are dropping people seem to be fixated with why they are still too high, and when prices are rising they are equally fixated with why they are still too low. We also note that the more fixated people are the more wrong they are, but enough of that, let us talk about the current market.

First we should mention that this is a discussion about prices in general as in every market there are companies that are over priced, companies that are under priced and companies that are reasonably priced. So what about today's prices? In both Canada and the United States, the markets have dropped around forty percent from peak to valley. Yet we continually hear about how based on earnings the markets are still high, as price earnings ratios (PE's) are still very high. Since the PE is calculated by dividing the share's price by its earnings per share, the higher the price in relation to earnings, the higher the PE. Since PE's are historically high, then so must be prices. This in itself brings up some interesting thoughts.

First, it is funny how when the markets were peaking no one seemed to care about earnings anymore. See Dave's Rule for more comments on this. We also believe that these concerns over high valuations are a bullish sign. Put another way, the more that people are worried that prices are too high, the more likely it is that they are actually too low. Something to do with the majority are usually wrong theory. Finally, we have noted that PE's are often excessively high just before a market run up. So let us discuss why this last peculiarity happens.

To some extent the markets mirror the economy. Actually, the longer the time period the more the correlation, as in the end, share prices will eventually reflect corporate earnings and corporate earnings will ultimately reflect the economy. That is, in general in a good economy earnings go up and in a recession earnings go down. Since earnings are what a company is in business to make, when earnings go up, ultimately so do stock prices, and when earnings drop so do stock prices. However, for a number of reasons, earnings will normally fluctuate a lot more than either the markets or the economy. Consequently, when stock prices are depressed, often corporate earnings are more depressed, resulting in rising PE's in a dropping market. This leaves the inevitable situation where people are nervous since the market is dropping and PE's are rising. As time goes on and the exaggeration increases, they get more nervous and often bail at the market bottom; then the cycle reverses.

As the economy improves so too do earnings and usually at a greater rate then either the economy or stock prices. After all, they have some catching up to do. As a result, PE's start to fall, even though prices are rising. This situation of depressed earnings is where we believe we are now. It is our expectation that when the economy rebounds, earnings will also rise but at a faster rate than either the economy or the markets. This is one of the two reasons why the current historically high PE's do not worry us.

The other reason is low interest rates. Return requirements on stocks are directly effected by the return on fixed income investments like government bonds. Investors will ultimately require a higher return on stocks than on more secure investments like government or corporate bonds. After all, why take the added risk if you do not expect a higher reward. Over the past few decades' investors have generally expected PE ratios of between 10 and 20. However, over this time period interest rates have been historically high. In recent years interest rates have dropped back to more historic rates where government bonds are only yielding returns of around 5 percent or less, and odds are these returns will not change significantly for some time. Since an investor cannot look for as high of returns from bonds, it stands to reason that they will not demand as high of returns on stocks as they had either. As a result PE's will likely be higher for some time to come.

So are prices too high? In general, not necessarily as earnings are probably somewhat depressed due to the current economy and PE's will likely be higher than they have been during the last few decades as interest rates and inflation stay in check.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: January 1995, January, 1996, September 1997, September 1998, September 1999, October 2001, October 2002, September 2009

As summer comes to a close and the fall leaves start to appear, it seems like a logical time to review your financial affairs. The first part of that is to review your asset mix and make sure it is still suited to your specific circumstances. To help you do this we try to reprint the following article once a year. We know that some of you have read it before, but we urge you to read it again, as this issue really should be revisited annually.

Balance, or asset mix, is probably the most important factor affecting your investments. Simply stated, it is the amount or percentage of your investments allocated to each type of investment. For example, an investor may have 40% of their investments in very safe investments like Treasury Bills, 10% in Medium safety investments like Corporate Bonds, 40% in equities and 10% in Speculative investments like an emerging market fund.

Getting the right mix is very important, but it is not always easy. The mix should consider all your personal circumstances and your personality.

Many planners have tried to simplify the task by creating canned approaches. Some are forms of market timing, others rely on formulas and still others rely on predetermined balances which seem to assume that everyone is the same.

One common formula is to deduct your age from 90, and the result is the percentage that should be in equities. Another recommends investing enough in fixed income investments to generate the income you need to live off, then putting the balance in equities. The problem is that these approaches assume everyone is the same. They do not consider your personality, risk tolerance, or even your long term needs.

Another approach is to time the markets. We have noticed that various timing services seem to keep cropping up. There is little question that successful market timing can provide terrific results. The problem is that these approaches have a way of letting us down when we need them most, and even if they do not, are you prepared to trust your future to short term market projections.

This leads us back to IFC Investment Principle number one; Balance your investments according to your personal circumstances. These other approaches may make your job or your financial planner's job easier, but they avoid tackling your most important financial decisions.

Two Kinds Of Risk

Before we go on we should discuss risk. When you are determining your balance you must consider the risk of the different investments. However, before you do, it is important to understand that for investors there are two types of risk. There is the risk of losing capital and of not having enough.

Most people are familiar with the risk of losing capital. It is what stops us from putting all our investments in speculative investments.

The other gets less consideration, but it may be the bigger risk. That is, the risk of not having enough money to live on, at an age when going back to work is not an option.

This leads us to the risk/reward equation. The main objective of balancing your portfolio is to find a mix that provides a reasonable return, and an acceptable level of risk.

Types Of Investments

Now that we have discussed risk, we are ready to look at the basic investment categories, their historic returns and their relative risk.

Very Safe Investments; These include investments such as deposit accounts, term deposits, guaranteed investment certificates, treasury bills, short term government bonds and short term government money market instruments. Over the long run they normally have the lowest return. Considering recent history, it is probably reasonable to expect long term returns close to the rate of inflation and one and one half times the rate of inflation.

Safe Investments; These include investments such as high quality short and medium term bonds, money market instruments, and mortgage instruments. While not as safe as the very safe investments, these are still considered very low risk. Generally when they show a loss it is small, temporary, and only a reflection of market conditions, not a weakness in the underlying security. These types of investments usually have long term returns that are slightly higher than the very safe investments.

Medium Safety Investments; These include investments such as long term government bonds, corporate bonds and bond funds. These investments are much more risky than either of the above two groups, although their greatest risk is market risk. While these investments can significantly out-perform or under-perform other investments, historically they perform only slightly better than the safe investments.

Equity Investments; These include investments in shares of companies. While they are considered riskier than any of the above investments, over the long term, they have shown the best results. Historically, the long term total returns of Canadian and U.S. equities have been over two to three times the rate of inflation.

Home Ownership; Most people greatly exaggerate the returns they earn on their principle residence. This is because they calculate the total growth in value and forget that it has happened over several years. Nonetheless, a house does provide an excellent hedge against inflation, a place to live (which saves you rent) and if it is your principal residence, any gains are tax free in Canada. In the long run, not many things can match the security of owning a home, once the mortgage is paid.

Now we can tackle some personal questions.

The Right Balance, A Personal Question

As we said earlier, obtaining a balance, or Asset mix that is right for you is probably the most important part of investing. This balance should not be influenced by the market. Once you have determined the mix, you should review it regularly, probably once a year, as times and circumstances change.

First you need to answer some personal questions.

1. What am I saving for?

2. What is my time horizon?

3. How much can I afford to lose?

4. Am I concerned about having enough?

5. How much risk am I comfortable with?

What am I saving for? Or what are your Goals? This will effect some of the other questions. Some common goals are; saving for the down payment on a house, your children’s education, a major purchase, to start a business, retirement, to supplement your income, and/or to generate an estate for your heirs.

Once you know your goals you are ready to answer the other questions.

What is my time horizon? How long do you expect to have the money invested? If your goal is a down payment on a house your horizon will probably be short. On the other hand, if it is for retirement, you might have a longer time horizon.

If your time horizon is short, say under ten years, you will need to concentrate on the lower return but safer investments. If it is longer, you can consider putting some money in the higher return but more risky investments.

How much can I afford to lose? We hate this question, but it helps to put things in perspective. Our circumstances and time horizons will play a major role here. While we do not want to lose anything, we can usually afford some losses. If you have a long time horizon or other income sources, you may be able to afford more risk.

The key question to ask yourself is what if you lose a substantial portion of your investments? Do you have time to rebuild or have other sources of income (e.g., salary or pension income). Consider your circumstances. The less you can afford to lose the more you should put in safe and very safe investments.

Am I concerned about having enough? This is a very important question. Playing it safe may be a route to the poor house. With the safer investments, after tax and inflation, it is very difficult to make money. So, living off the interest may not be an option. For many, their biggest fear should be running out of money.

How much risk am I comfortable with? A truly personal question. This is one of the main reasons that we do not like canned formulas. Two people in exactly the same circumstances should not necessarily make the same decisions. We are, after all, human. The amount of risk, not to mention volatility, you are comfortable with is a factor of your personality, experience, upbringing and exposure. You have to take a good look at yourself.

Sometimes we recommend that a client invest a lower percentage in equities than we feel is appropriate, because we know they are not comfortable with risk. However, as they gain experience, we are often able to increase the amount of equities to more appropriate levels. On the other hand, there are also those who cannot sleep at night if they do not have significant holdings in equities. They do not like knowing that their investments have little or no opportunity for real growth. You need to know yourself.

Selecting The Balance

Once you understand the different types of risk and different types of investments, and have asked yourself the above questions, you are ready to determine your investment balance. This can be done by investment category.

Very Safe and Safe Investments; For most people these should make up between 25% and 75% of their investments.

If you have a short time horizon, are concerned about loss of capital or are not comfortable with the volatility and risk of equities, then this group should make up a high percentage; closer to 75%.

If you have a longer time horizon, say ten or more years, you can afford some setbacks, and can live with some volatility and losses, then the amount invested in these types of investments can be lower.

Medium Safety Investments; For most people these should make up between 0% and 50% of all their investments.

Some people have had very good results in this area, especially in the last couple of decades. However, in our opinion, the historic returns do not justify large investments in this area. Also, these investments do best when interest rates are dropping. Not something that is likely to happen in a big way right now.

Equity Investments; For most people these should make up between 25% and 75% of their investments.

Historically they have the best returns, but they are also the most volatile. If you are looking for growth, this is the place to look. However, since it is the most volatile, all the money invested in this area must have a long time horizon. We prefer a minimum of ten years.

If liquidity is not important, you have a long time horizon, can afford setbacks, and you can live with the ups and downs, then the percentage in equities should be on the higher side. Also, if you are concerned about inflation or having enough money to retire on, a reasonable equity portion is necessary.

If you meet the criteria for a large equity portion, but lack experience with equities, you might want to lower the percentage until you have gained some experience and lived through some market setbacks.

Some Final Thoughts On Equities; Diversify, diversify, diversify, otherwise you leave yourself open to holding one big loser. The idea is to have a healthy mix where in the long run the winners will more than make up for the losers.

International Equities; We recommend you place at least 30% of your equities in companies that do business around the world. This will provide exposure outside Canada and further spread your risk.

Conclusion

Selecting the proper balance is one of the most important parts of investing. You need to review your personal circumstances, the types of investments, and then select a mix that is suitable for you.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: July 2002

OKAY, we have heard enough of this "things are different now and you need to trade to make money in this market"…. crap. This is pure bunk. You need to trade if your goal is to make money for your broker, but in our opinion that is the most positive effect you are likely to achieve. If your broker tells you this, FIND ANOTHER BROKER. If your portfolio manager or fund manager says this, FIND ANOTHER MANAGER. If your advisor tells you this, FIND ANOTHER ADVISOR. If you hear this in locker rooms or chat rooms and you pay attention, then you deserve what is coming to you for being foolish enough to listen to anything you hear in either locker or chat rooms.

Do we sound a little fed up? Well you are dammed right we are, and this crap is just going to far. In 1999 they said you had to buy technology, ignore profits and all the old rules because everything has changed. We continued to warn our readers that nothing had changed, but who listened? Now we are hearing the line that in this flat market, you need to trade as things have changed. Well we are here to tell you again that nothing has changed; the old principles and rules are as true now as they have ever been. If you doubt us even a little, then it is time to take this link and read or reread our January 2000 issue of Financial Insight.

In the long run, and investors should be long run thinkers, sound companies, with good profit histories, good potential and good management will grow, prosper and reward their owners. As long as this is the case, they will continue to prosper and grow, so there is little need to sell them. Yes the ride will be a bumpy one, but the trend will be up. If your portfolio is made up of this kind of company, most of your holdings will eventually reward you. Different companies will reward you at different times but over the long term (5 to 10 years) most of them should pay off. Then there is the bonus, as long as most them are still good companies they will continue to grow over the long term, so you will probably want to keep most of them and only sell when the circumstances or your opinion of a company changes or when one has done so well that it makes up a disproportionate amount of your portfolio, in which case you might wish to reduce your holdings.

You can make a lot of money trading if you get it right, or lose a lot if you get it wrong. It is our view that it is a lot easier to select good companies and build a solid portfolio then to second guess the temporary moods of the market. You will still make mistakes, but chances are that in the long run you will make more right decisions and those right decisions will more than make up for the mistakes. It might not be exciting, it will not make your broker rich and you will not be the most interesting person in the locker room, but in the long run you might turn out to be the most successful investor. So what is your goal, short run glory or a sound long-term overall return?

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: July 2002

The price earnings ratio, (often referred to as PE), is a company's share price divided by its earnings per share. This is a very popular and useful tool for measuring value or share price. The higher the PE the higher the share price is in relation to earnings and the more likely that the price is overvalued. Unfortunately, what is often forgotten is that the ratio is a factor of both share price and earnings.

As long as the earnings number being used is reasonable, then the PE is likely a fairly good measure of share price. The problem is that in the short run, even for the best companies earnings sometimes fluctuate from the overall trend. These fluctuations can be a result of many things, but one time items and economic factors are among the most common problems, and while they can and often do effect current earnings to a much greater effect than the market effects share price, they may not be very relevant to the company's long term financial health and therefore its real worth. Let us explore an example.

Let us say that company "A" has been growing its earnings at 10% per year fairly consistently for several years, that we would normally expect a PE of 10 for the company and that all things being equal this years earnings should be $1.00 per share. Then a reasonable share price would be $10.00. The PE of 10 times the earnings per share of $1.00. So let us assume that the price is 10.00 and everything is fine. But what if the company had a fire so its plants were closed for nearly half the year. We will also say that insurance paid to restore the plant and now everything is running smoothly again, and that chances are that in a year or two earnings should be back on the old track. In this case $10.00 is still a fair share price. However, for a year or two, earnings were cut in half due to lost sales (not covered by insurance) because of the fire. So current earnings are only $0.50 per share. So at $10.00 the PE is now 20 times, twice the expected PE for the company. Thus, according to the PE ratio, at $10.00 the share price is way to high. More likely, because of the situation, the share price would drop. Let us assume it dropped to $7.00. From a long run point of view, this is a very attractive price, and if it were not for the fire there would be a very attractive PE of 7. However, if you do not look carefully at earnings, you will see a PE of 14. Seven dollars divided by the current real earnings of $0.50. In this case you might find yourself selling when the price is at its lowest rather than taking advantage of a buying opportunity.

Other similar examples could include temporary earnings reductions due to economic factors, restructuring costs, a slowdown due to plant restructuring, one time write downs or any number of things. Alternatively, one time opportunities might cause a company's earnings to be over inflated one year, which could distort the PE by making it lower than it would be, had you removed the one time factor.

So while we often look at PE's to value stocks, and markets for that matter, it is important to understand the make up of those earnings. Sometimes, due to the higher fluctuations in earnings, you may not be aware that a high PE is actually an indication of a low price rather than the normal situation that is the opposite. This is especially true in the case of valuing markets during times of recession. So before you jump to any conclusions based on PE's, make sure you know what makes up the earnings number.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: March 1997, April 1998, March 2002

Note: The following article applies to Canada, but investors in any country should consider the principles. While the conclusions may differ in different countries, you should still consider them in your investment strategy.

Our standing advice is to place about thirty percent of your investments in international investments. For the equity portion of your portfolio, this can be a portfolio of shares from all over the world, a portfolio of North American companies that do business around the world, or a mix. Of course the shares can be held individually, in mutual funds or in both. This advice is meant to reduce risk by spreading it over several economies. The problem comes when people invest too much outside their own country.

With a federal debt of almost 600 billion dollars (about $20,000 per person), massive provincial debts, a federal pension scheme that may or may not prove to be sustainable, an unsustainable health care system that many seem bent on maintaining, and in reality, a one party federal so called democratic system, it becomes easy to see why the Canadian dollar is continually eroding and why many investors wish to hold a large portion of their investments outside Canada.

If Canada does not get its act together, these foreign investments will pay off. They will provide increased stability and when converted to Canadian dollars, their value will be even greater. Actually, this is a main reason why we recommend some foreign content.

But what if they are wrong? Maybe they are taking a good thing too far. Few of these investors plan to leave Canada, so their welfare is connected to it, and they will ultimately need Canadian currency.

When you think about it, putting most of your investments outside Canada is a bet against the Canadian dollar. If your returns are good and the dollar goes down, you get a double pay off. However, if the dollar improves by ten percent (ten percent equals about six cents) the value of your investments will drop about nine percent. Your foreign growth could actually be eroded by exchange losses. Many people doubt this will happen, and while we will agree that there is a significant chance that it will not happen, we also think that it is entirely possible that it will happen.

While there are serious concerns, there are also reasons to be bullish about Canada in the long run. Compared to the American currency, the Canadian dollar is historically low. As the different economies all over the world gain momentum, especially the third world economies, we believe that Canadian expertise, knowledge and resources will be called upon. As a result of the war on terrorism, it appears, as we suspected it would, that Canada's ties with the United States will ultimately strengthen, promoting increased trade. For some time now Canada has had a trade surplus, which will ultimately mean increased demand for our currency. While there is a huge amount of government debt, the federal government has managed to get into a surplus position and is starting to reduce its debt. Also, most provinces have stopped running deficits and one may even eliminate its debt in this decade. We shall see if the Canada Pension Plan is sustainable, but at least there is now a plan and plans can be modified. As for health care, emotions run deep, however, in the end practicalities will force us to figure out what needs to be done and to make the necessary changes, whether we like them or not.

So while there is cause for concern about the Canadian economy and our currency, there is also a lot of reason to be optimistic. What this means is that we need to manage our investments for either eventuality. The best way to do this is to have a reasonable portion of our investments in foreign investments, but not to overdue it. This way if Canada does poorly, we will have some foreign coverage to protect us. If we hold our own, then the foreign content will not hurt either and if Canada does flourish, well since most of our investments are in Canada, we are bound to prosper as well. Now that is reasonable diversification, in all its glory.

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: March 2003

First let us set the record straight. The Enron case is nothing new, different or unusual. In fact, you can predict a similar story will happen again in three or four years, then again in another three or four years, then again in another ....... well you get the picture. What should be surprising (should be but is not) is how it is always treated like a surprise and as if because of this amazing story, everything has changed. Automatically names like Dome, Principle Trust, Bre-X and Long Term Capital come to mind. The fact is that every few years a major hot stock crumbles. While we can learn some lessons from each, and each one will influence future investing in its own way, these stories are to be expected in any free enterprise system. But we should also remember, they are the exception, not the rule.

Obviously, it is in our interest to avoid these catastrophes, so rather than lose sleep over what has happened, or what will happen, we should concentrate on how to avoid having them happen to us. Following are some things to watch out for when you are picking stocks. Be careful though, there are no hard and fast rules. It is important to look at the whole picture and put any warning signs in perspective. We expect that most of the best companies will appear to exhibit some warning signs from time to time, and depending on the circumstances, the same sign may be a positive factor in one case and a negative in another. Now that we have shattered your confidence, we should bring up the most important safeguard.

Your best defense is always to build a solid well-diversified portfolio of high quality stocks. It may be true that the more stocks you hold the more likely you are to own the next Enron, however, by concentrating on quality we reduce our risk and by being satisfactory diversified (but not necessarily over diversified) we limit the damage that can be done by any one stock, sector or region. We also increase the odds that our winners will more than make up for our mistakes, and rest assured, there will be mistakes.

So here are some things to consider when selecting stocks:

Return to top of page.

Return to Financial Insight's main page.

![]()

Published: April 1998, October 1998, January 2002

Derivatives can mean a lot of things, but here we are referring to options and futures contracts. Essentially, an option is an agreement where one party gets a fee to agree that up until a certain date, the other party can purchase from them (a call option) or sell to them (a put option) a specific security for a predetermined price. Essentially, a futures contract is where two parties agree that one will sell a given security or commodity to the other party at a specific date for a specific price.

Options: In the case of an option one party is speculating that the price will not be reached while the other is speculating that it will be. Many small investors use this as a method of leveraging a small amount of money. They will buy a call option for a small fee. If the price goes up they can either sell the option for a profit or call the option and immediately sell the security without putting up the full amount themselves. Since the option fee is a fraction of the cost of the security, they stand to make a very good return on their investment. Of course if the price is not met, they lose the whole investment. A put works in reverse, they hope the price will drop so they can buy it for less and immediately sell it to the seller (writer) of the put option.

The person selling the option is often a larger investor who is also speculating. They are gambling that they will get the fee but the option will not be exercised. If they are right, and they usually are (we have heard that as many as ninety percent of options do not get exercised), they make a tidy little profit. If it is a call option and they already own the stock, then there is little risk. Except that if they are forced to sell a good stock, they could lose a substantial amount of growth if the market goes up quickly.

The above is how investors speculate using options, something we do not advocate, as in the long run, the real winners are usually the brokers, not the investors. However, options can be used as a hedge to reduce your risk. Say for example, you knew that you were going to receive a security in the future, but you were concerned that the price might drop before then. You might buy a put option. Then you would know that if the price dropped, you could still sell the security at the put price. In this case, for a small fee you have removed the risk of seeing a large drop in price before you take delivery. On the other hand, if you were expecting a large sum of cash in the future, but were concerned that the price of a security you want might go up before you have the money, you could remove the risk by buying a call option. Then if prices rise before you get the money, you know that you can still buy the securities for the predetermined price.